When you're diving into the world of algorithmic trading, one of the most important steps you can take to ensure success is backtesting. So, what exactly is backtesting? Simply put, it’s the process of testing your trading algorithm on historical market data to see how it might have performed. It’s like running a video game simulator for your trades before you go live and risk real money.

If you're new to this, no worries—start with our Algorithmic Trading 101 blog post for the basics. In this post, we'll break down what is backtesting, why it's a game-changer for algo trading success, and simple best practices for backtesting trading strategies. Let's make your next trade smarter, not harder.

The main reason backtesting is a must in algorithmic trading is that it allows you to simulate how your trading strategy would perform, without taking any real financial risk. After you designing an algorithm based on a strategy you think is great—backtesting is the quick check to preview its potential effectiveness. We think it's essential for a variety of reasons:

Validate Your Ideas Fast: A strategy that works on paper might fail in the real world due to changing market conditions, or unforeseen events. Backtesting lets you test your strategy on real historical data, helping you see if the rules you’ve set could lead to profitable trades or if they need adjusting.

Handle Real-World Chaos: Understand how your algorithm behaves in different market conditions by testing against diverse historical datasets, such as bull and bear markets. Markets are constantly shifting, and how your algorithm performs during volatility, sudden drops, or rising trends provides a clearer picture of its potential.

Build Around Risk: By testing on historical data, you can spot potential flaws or weaknesses in the strategy and address them, though rare, unpredictable events may still pose challenges. Finally, it lets you optimize performance by tweaking settings like entry/exit points and stop-loss levels to maximize profit. You can read more about risk reduction on our blog post “Top 10 Risk Management Tips for Algorithmic Traders.”

Boost Your Confidence: Live trading can be nerve-wracking, and knowing your algorithm has been tested against historical data offers peace of mind. When backtest results show consistent past performance, you can stress less, and focus on what matters.

While backtesting is crucial, following best practices ensures accurate and reliable backtest results.

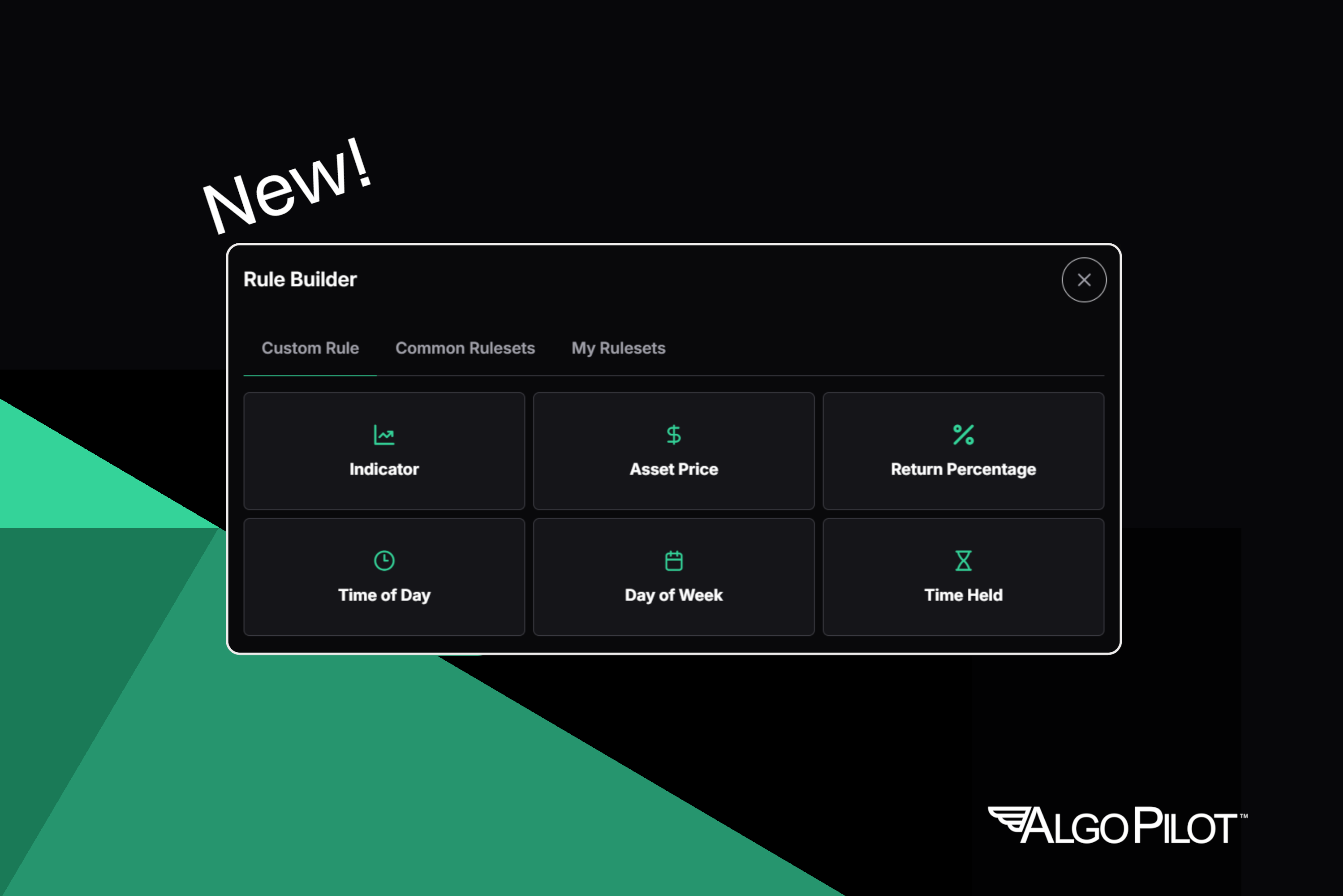

Quality Data: Start with clean, accurate data from trusted sources—such as brokers or financial data providers—that reflects real market conditions, including price movements and trading volume. Platforms like Algo Pilot simplify this process by providing quick access to high-quality historical data.

Dodge Overfitting Traps: Overfitting occurs when you tweak your algorithm too closely to past data (e.g., adjusting it to fit a specific market trend like 2020 crash or 2023 boom) making it less effective for future, different conditions. This can create unrealistic performance expectations. To avoid overfitting, test your algorithm on datasets from different time periods.

Simulate Multiple Scenarios:Testing across different market conditions (i.e., bull, bear, or especially volatile periods) is crucial. Tools like Algo Pilot make this easier by allowing you to simulate various scenarios just by editing a date setting and re-running the backtest to compare results against each other. For a bit more advanced user, a walk-forward testing approach can help ensure adaptability and reduce overfitting.

Factor in Real Costs:Don’t forget to account for transaction costs (e.g., fees) and slippage (price changes during trades) when running backtests. While Algo Pilot never charges variable fees, some platforms and typically your broker will.

Measure it: Don’t rely on just one metric like total profit. Consider Win Rate, Drawdowns (losses in value), Sharpe Ratio or risk-adjusted returns, and consistency. Algo Pilot provides an intuitive, and user editable, layout to view backtest metrics easily.

Backtesting is powerful, but it’s not magic. Historical data may not capture rare events, and data biases or incomplete records can skew results. Computational power can be a constraint. Use it as a guide, not a definitive predictor.

That's why we love paper trading as a next step. Paper trading (offered by some brokers) is simulated live trading that allows you to see what your algo would do under current conditions, but without the risk of loss of capital since you are not actually trading real money.

Backtesting is an absolutely crucial part of algorithmic trading. It allows you to assess your algorithm’s potential and guide adjustments without risking actual money. By following best practices (like using high-quality data, avoiding overfitting, accounting for costs, and testing across conditions) you’ll improve your chances of success. Remember, it’s not a guarantee, but a powerful tool to navigate algorithmic trading’s complexities. With Algo Pilot, you can continuously refine your strategy for better real-world performance.

Algo Pilot® is a US based technology company and not a bank, broker-dealer, or RIA. As such, Algo Pilot LLC does not provide investment advice and is not a member, SIPC. Brokerage services offered by 3rd parties are not directly affiliated with Algo Pilot LLC, and Algo Pilot® users may choose the broker relationship that they desire.

Past performance, whether actual or indicated by historical tests of strategies, is not a guarantee of future performance or success. Investing in stocks, futures, options, currencies, cryptocurrencies, and other financial vehicles involves risk. Investing in securities involves potential loss of principal. Trading in options or security futures involves a high degree of risk and investors may lose more than their initial investment; options trading is not suitable for all investors. Before trading, please read all applicable risk disclosures such as Characteristics and Risks of Standardized Options disclosure from your broker.

Algo Pilot® is a registered trademark of Algo Pilot LLC. Algo Pilot's Algo Builder is Patent Pending with the USPTO.